1929, storytelling and investments

- 12 hours ago

- 5 min read

"There can be few fields of human endeavour in which history counts for so little as in the world of finance." — J.K. Galbraith

A recent podcast guest (The CIO Chair) guest suggested reading "The Great Crash 1929" by John Kenneth Galbraith. This is a finance classic written in 1955 and chronicles the actors and actions of the Wall Street Crash. It is hard not to see the parallels with the exuberance we are living through. This week's blog is about the stories we tell ourselves, or that others tell us to make sense of the situation.

Galbraith identifies, three essential parts of the last run-up in prices:

Borrowing money to fund the purchase of investments

Expectation that they will sell when prices rise

Wildly optimistic storytelling to justify current and future prices

These three spell out huge levels of undisciplined speculation. When people buy assets on borrowed money, at punchy valuations on the expectation they will rise so they make a quick profit, we have the perfect set-up for giddy price rises and then an inevitable collapse. It feels we are getting close to that point now.

Last week I wrote about motivated reasoning (Feeling, then reason). This is when we have a strong incentive to arrive at a specific conclusion and torture the available evidence until it supports our wishes. In these giddy times, there are many storytellers who have to make the numbers support the argument.

We like to think we invest rationally. But we can get ourselves into trouble by following crowds. Whilst I will leave predicting recessions, bear markets and credit crises to the many people who fill the 24/7 financial media, you can't help but think that the stories being told right now feel out-of-the-ordinary optimistic.

Although I have not seen it with my own eyes, apparently the spreadsheet used to justify the SpaceX (SpaceX IPO Roadshow.pdf) valuation had the AI division revenues alone of $300bn within 10years. For a company with currently $20bn total revenue, it requires a lot to go right to get there.

Stories follow prices

The Forbes cover curse, is an incredibly reliable indicator. The joke goes that you should short a stock once the CEO appears on the cover of Forbes. The common assumption is that newspapers provide a bullish news story and then investors buy the stock. i.e stories drive prices. I think it is mostly the other way round. The price moves first and only then is the story constructed afterwards to justify it. The incentive of a newspaper is to make the price move that just happened look inevitable.

Financial ecosystems create self-fulfilling moves. The price rises -> financial media highlights the price rise with an optimistic story -> other investors hear about the price rise and buy -> the price rises and so on. This is also true on bearish moves.

This way round we understand why stories are most optimistic when prices are at their highest. The company must be amazing at that price right?

As we covered earlier, numbers rarely protect us. Forecasts require assumptions on growth rates, margins and terminal values. All of these numbers can be made up based on bullish assumptions.

Some fairytale stories work, many do not

Hall of Fame | Hall of Shame |

Apple | |

Amazon | Peleton |

Netflix | WeWork |

Nvidia | Cisco |

Meta | Worldcom |

The hall of fame and hall of shame were companies that had hockey stick projections against them. Whilst we all know what happened next, all the companies were meant to change the world, operating in unique ways that guaranteed future success. At the start of these journeys cheerleaders convinced us that at even theses nosebleed prices was cheap. Similarly the bears (probably native fixed income investors!) said that these companies would struggle to justify. Both cheerleaders and bears were right 50% of the time from those lists.

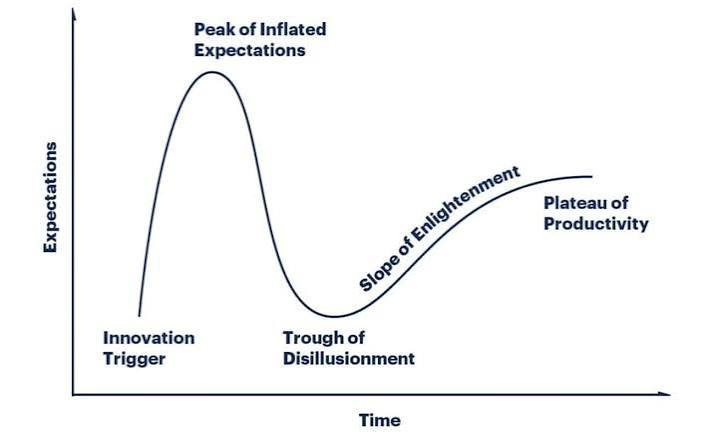

Although uncomfortable it requires to humility to accept that in a heady time the two lists sounded almost identical i.e. being always bullish or bearish is not a winning strategy. I do think though, there are times particularly where we are excited about a new technology to such an extent that we have inflated expectations. On the Gartner hype cycle below, I think AI is approaching the Peak of Inflated Expectations from a valuation perspective.

What you need to believe

A habit from my years in fixed income. Strip any investment back to one question: what do I need to believe for this price to be right? The downside gets most attention as our upside is capped.

In each investment there is an inherent story. For equities it tends to be sustainable growth, for credit its more about stability to pay interest, for commodities it might be about supply constraints and crypto about future adoption. My contention is that we fit the story and model to our feelings and the price rather than what is in front of us.

Five storytelling frenzy indicators

If stories follow prices, then the stories themselves are an indicator. Here is an attempt at five:

Profitless outperformance. Companies with no earnings beating companies with earnings.

Metric dilution: cash flow -> P/E gives -> price-to-sales -> price-per-user, then -> share of a "total addressable market". You are no longer asked to believe next year's earnings but something a generation away.

Valuation and Rating "negotiation". Ratings, audits and valuations become negotiable. Independent verification is avoided.

Retail are given access at the top of the market: Access to the hottest assets are suddenly opened to everyone.

Leverage. Buyers are accessing the market on leverage or through derivatives.

None of these are timing flags, but it does help you gauge whether "tourist" capital may be subject to unwind on price declines.

There is an old Wall Street line that bear markets return assets to their rightful owners. In the next downturn, whenever it comes, we will find out who was speculating on leverage, which companies were committing fraud and people who were mis-sold to.

So what?

Stories follow prices rather than prices following stories. Optimistic at the highs, pessimistic at the lows.

Numbers are constructing to support the story. Forecasts, multiples and ratings can be skewed by euphoria.

Optimistic stories are not automatically wrong. Amazon and Nvidia grew into nosebleed valuations. But we remember the winners and forget the losers, which flatters the odds.

The frenzy indicators: profitless outperformance, metric migration, valuation/rating massaging, retail participation and leverage. All are present today. What that means for timing, who knows.

Bear markets return assets to their rightful owners. Until then, the sceptic and optimist should humbly ask the same question: why might I want this to be true?

Next week, will be "Certificates versus the proof of work". As always get the blog delivered directly to your inbox on Home | Deciders | for mental fitness | change your mind.

Comments